What Is A Second Mortgage?

If you’re a homeowner looking for financial flexibility or considering renovating your home, a second mortgage can be a viable option. In this article, we will explore the concept of second mortgages in easy-to-understand language while What Is A Second Mortgage?

Second Mortgages

First, let’s break down the basics. A second mortgage is a loan that is secured against your home, in addition to your primary or first mortgage. This means your home is used as collateral to secure the loan. In case you default on the loan, the lender has a claim on your property.

What Exactly Is a Second Mortgage?

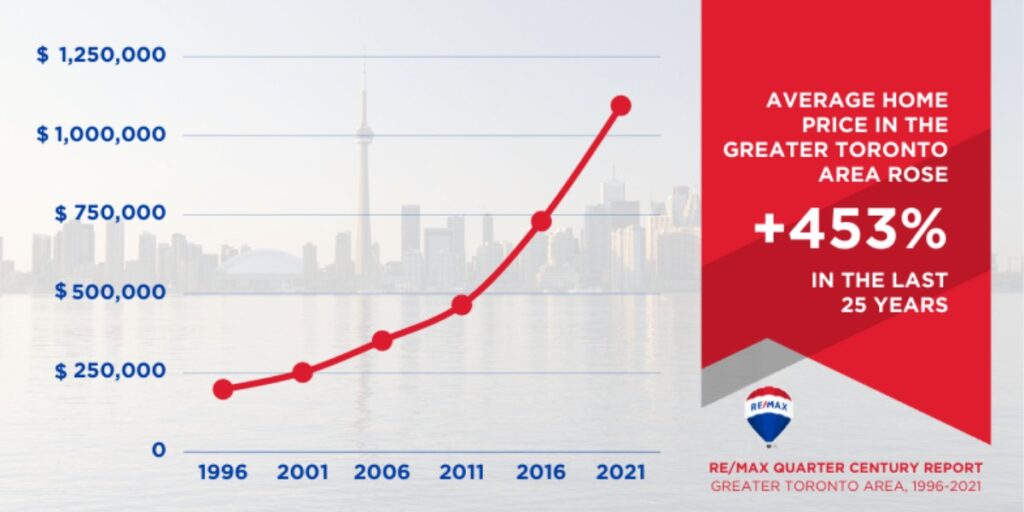

A second mortgage is essentially a way for homeowners to tap into the equity they’ve built in their property over time. Equity is the difference between the current market value of your home and the outstanding balance on your primary mortgage.

Types of Second Mortgages

There are two primary types of second mortgages: home equity loans and home equity lines of credit (HELOCs). We’ll explore the differences and benefits of each in the upcoming sections.

Differences Between a Second Mortgage and a Home Equity Loan

Many people use the terms “second mortgage” and “home equity loan” interchangeably, but they’re not quite the same thing. We’ll clarify the distinctions between these two financial tools.

When Might You Consider a Second Mortgage?

Second mortgages can be useful for various financial purposes, from home renovations to debt consolidation. We’ll delve into common scenarios where obtaining a second mortgage makes sense.

How Does a Second Mortgage Work?

Understanding the inner workings of a second mortgage is crucial. We’ll explain the process, interest rates, and loan terms associated with this financial product.

Benefits of Getting a Second Mortgage

Second mortgages offer several benefits, including lower interest rates compared to credit cards and the potential for tax-deductible interest. We’ll discuss these advantages in detail.

Risks Associated with Second Mortgages

No financial decision comes without its risks. Second mortgages can lead to financial strain and put your home at risk if not managed responsibly. We’ll address these potential pitfalls.

Qualifying for a Second Mortgage

Securing a second mortgage depends on various factors, such as your credit score, income, and the amount of equity in your home. We’ll guide you through the qualifications.

Second Mortgage vs. Refinancing

Some homeowners may wonder whether refinancing is a better option than obtaining a second mortgage. We’ll compare these two alternatives to help you make an informed choice.

The Process of Obtaining a Second Mortgage

Getting a second mortgage involves paperwork and financial assessments. We’ll provide a step-by-step guide to help simplify the process.

Second Mortgages and Your Credit Score

Your credit score plays a crucial role in obtaining a second mortgage. We’ll explain how your credit history impacts your eligibility and interest rates.

Is a Second Mortgage Right for You?

In the final section, we’ll help you assess whether a second mortgage aligns with your financial goals and needs. Weighing the benefits and risks, you’ll be better equipped to make an informed decision.

In summary, second mortgages can be a useful financial tool, but they come with responsibilities and potential risks. By understanding how they work and evaluating your individual circumstances, you can determine if a second mortgage is the right choice for you.

Click here for more visited Posts!