Canadians Consider Splitting A Mortgage With Friends. But It’s Complicated

Shared Mortgages

Buying a home is a significant milestone for many Canadians, but the soaring costs of real estate can make it challenging to achieve this dream alone. Canadians Consider Splitting A Mortgage With Friends. But It’s Complicated. In response to this financial hurdle, an increasing number of Canadians are considering the option of splitting a mortgage with friends or family members. While this arrangement can offer financial advantages, it also comes with its own set of complexities and considerations.

Understanding the Concept of Splitting a Mortgage

Splitting a mortgage involves multiple individuals coming together to jointly purchase a property and share the financial responsibility of repaying the loan. Instead of relying on a single income to qualify for a mortgage, co-borrowers combine their resources to meet the lender’s requirements.

Pros and Cons of Sharing a Mortgage

One of the primary benefits of sharing a mortgage is the ability to afford a more expensive property than what might be feasible individually. Additionally, sharing expenses such as down payments, closing costs, and ongoing mortgage payments can significantly lighten the financial burden for each party involved. However, shared mortgages also entail risks, including potential strains on personal relationships, disagreements over financial matters, and complications in the event of one party wanting to exit the arrangement.

Financial Benefits of Splitting a Mortgage

By pooling financial resources, co-borrowers can access better mortgage terms, including lower interest rates and more favorable loan terms. This can result in substantial savings over the life of the mortgage and make homeownership more affordable in the long run.

Legal and Emotional Considerations

Before entering into a shared mortgage agreement, it’s crucial for all parties involved to consult with legal and financial advisors to understand their rights and obligations. Clear communication and transparency are essential to mitigate potential conflicts and ensure that everyone is on the same page regarding financial expectations and responsibilities. Additionally, it’s essential to consider the emotional dynamics of sharing a significant financial commitment with friends or family members and how it may impact relationships over time.

How to Decide if Sharing a Mortgage is Right for You

Deciding whether to share a mortgage requires careful consideration of various factors, including financial stability, long-term goals, and personal dynamics. Individuals should assess their comfort level with risk, their ability to communicate openly and honestly with potential co-borrowers, and their willingness to compromise on financial decisions.

Tips for Finding Compatible Co-Borrowers

Finding the right co-borrowers is crucial to the success of a shared mortgage arrangement. Ideally, individuals should seek out friends or family members who share similar financial goals, values, and communication styles. It’s essential to discuss expectations, financial habits, and long-term plans upfront to ensure compatibility and minimize potential conflicts down the line.

Establishing Clear Agreements and Responsibilities

Before finalizing a shared mortgage agreement, it’s essential to outline clear expectations and responsibilities for all parties involved. This includes detailing how mortgage payments will be divided, who will be responsible for property maintenance and repairs, and what procedures will be followed in the event of disagreements or changes in circumstances.

Potential Risks and Challenges

While sharing a mortgage can offer financial benefits, it also comes with inherent risks and challenges. These may include disagreements over financial management, changes in personal circumstances (such as job loss or relocation), and the potential impact on credit scores and financial stability.

Alternatives to Shared Mortgages

For those hesitant to enter into a shared mortgage agreement, there are alternative options to consider. These may include purchasing a smaller or less expensive property, exploring government assistance programs, or entering into a rent-to-own arrangement.

Exploring Shared Ownership Models

In addition to sharing a mortgage, individuals can also explore shared ownership models such as co-housing, co-op housing, or real estate investment trusts (REITs). These arrangements offer different levels of financial and legal responsibility and may better suit the preferences and circumstances of certain individuals.

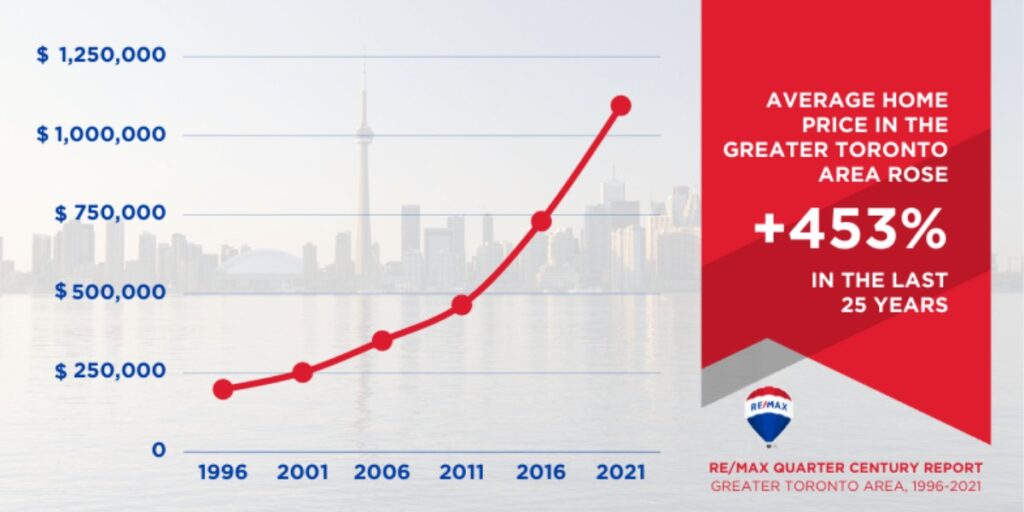

The Canadian Perspective on Shared Mortgages

In Canada, shared mortgages are becoming increasingly popular, particularly in cities with high housing costs such as Toronto and Vancouver. However, it’s essential for Canadians to approach these arrangements with caution and to seek professional advice to ensure that they fully understand the implications and risks involved.

Making Informed Decisions About Shared Mortgages

While splitting a mortgage with friends or family members can offer financial advantages and make homeownership more accessible, it’s not a decision to be taken lightly. Before entering into such an arrangement, individuals should carefully weigh the pros and cons, seek expert advice, and establish clear agreements and responsibilities to protect their interests and minimize potential conflicts. By approaching shared mortgages with diligence and foresight, Canadians can navigate this complex financial decision with confidence and achieve their homeownership goals.

Click here for more visited Posts!