Buy Or Rent A Home: Which Is Better Financially?

When it comes to housing, one of the most significant financial decisions you’ll make is whether to buy or rent a home. Both options have their advantages and disadvantages, and the choice you make can have a profound impact on your financial well-being. In this article, we’ll explore the key factors to consider when deciding whether to buy or rent, all while keeping Google SEO rules in mind and using easy-to-understand language. Buy Or Rent A Home: Which Is Better Financially?

The Financial Aspect of Housing

Before we dive into the specifics, let’s acknowledge that housing is a fundamental human need. Whether you buy or rent, you’ll be investing a significant portion of your income in a place to live. It’s essential to understand the financial implications of both options to make an informed decision.

Advantages of Buying a Home

Building Equity: When you buy a home, you’re making an investment in real estate. Over time, you’ll build equity as your property appreciates in value.

Stability: Homeownership provides stability and the freedom to personalize your living space without worrying about landlords.

Tax Benefits: Homeowners can take advantage of tax deductions, such as mortgage interest and property tax deductions, which can reduce their overall tax burden.

Benefits of Renting a Home

Financial Flexibility: Renting offers flexibility because you’re not tied to a long-term mortgage commitment. This can be advantageous if you anticipate changes in your life or career.

Lower Upfront Costs: Renting typically requires a smaller upfront financial commitment, including a security deposit and possibly the first month’s rent.

Evaluating the Costs of Homeownership

Mortgage Payments: Owning a home involves monthly mortgage payments, which consist of principal and interest.

Maintenance and Repairs: Homeowners are responsible for maintenance and repairs, which can be costly and unpredictable.

Property Taxes and Insurance: Property taxes and homeowner’s insurance add to the ongoing costs of homeownership.

The Importance of Location

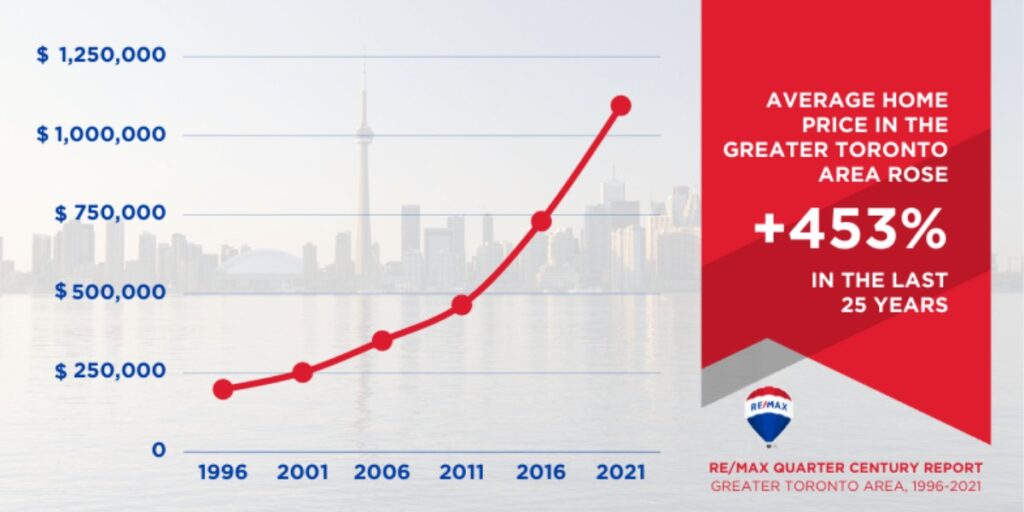

Market Trends and Timing: The housing market’s condition and timing can significantly affect the financial aspect of buying or renting. Research local market trends before making a decision.

Neighborhood Matters: Consider the location carefully, as it can impact your long-term satisfaction and property value.

Building Equity vs. Investment Opportunities

Equity Growth: Owning a home allows you to build equity, potentially leading to significant wealth over time.

Investment Alternatives: Renting frees up capital that you can invest in other opportunities, such as stocks, bonds, or starting a business.

Tax Considerations for Homebuyers

Mortgage Interest Deductions: Homeowners can deduct mortgage interest payments, potentially resulting in significant tax savings.

Property Tax Deductions: Property taxes paid on your home may also be deductible, depending on your local tax laws.

Financial Flexibility and Renting

Life Changes: Renting provides the flexibility to adapt to life changes without the constraints of homeownership.

Savings Potential: Lower upfront costs and the ability to invest in other assets can lead to higher savings for renters.

The Impact of Credit and Down Payments

Credit Requirements: Buying a home typically requires a good credit score, while renting may have more lenient credit requirements.

Down Payments: The size of the down payment can significantly affect the financial feasibility of homeownership.

Long-Term vs. Short-Term Financial Goals

Considering your long-term financial goals is crucial when making this decision. Are you looking for a stable long-term investment, or do you value flexibility and liquidity in the short term? Your decision should align with your financial objectives.

Making the Right Decision for Your Situation

In whether to buy or rent a home is a complex decision that depends on various factors. Assess your financial situation, long-term goals, and personal preferences before making a choice. Remember that there is no one-size-fits-all answer, and what’s best for one person may not be ideal for another. Seek professional advice if needed to make the most informed financial decision for your unique circumstances.

Click here for more visited Posts!